2022 is certainly hard to get better or worse from here

In this article, we explored the causes of recent volatility and future scenarios where investor sentiment may improve.

Thursday, October 6, 2022 at 11:33 AM

Castle Point Fund Management

Stephen Benny

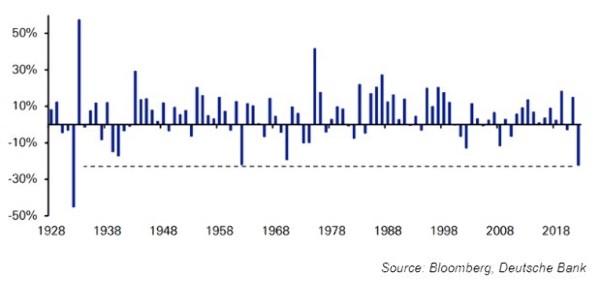

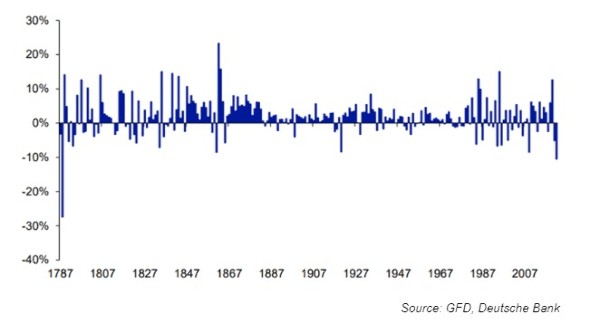

First, we have some good news. History shows that the stock market always recovers from drawdowns and eventually continues to hit all-time highs. But so far, there’s no getting away from the fact that 2022 has been a tough time for investors in most asset classes. Both bonds and stocks plummeted. Stock markets in most developed countries plunged into bear market territory in June, down more than 20%. It’s been countless decades since the stock market got off to such a bad start. And it’s been centuries since the bond market got off to a bad start at the start of the year, the 1700s to be exact.

A chart showing the start of the S&P500’s worst year since the 1930s

Chart Showing Worst New Year for 10-Year Treasuries Since 1788

Times like these can be especially difficult for investors in our part of the world. As investor sentiment deteriorates and stock prices around the world become more correlated with markets, business fundamentals temporarily become irrelevant. What matters most is what the S&P500 does overnight, and that determines the market’s performance for the day. At least American investors can wake up and hope that the day is going to be a better day for their stock portfolios. I know it’s going to be a bad day for stock portfolios. It can become a depressing spiral. It’s a very weak Friday, especially in the US stock market, and you can spend the whole weekend knowing that a bad Monday starts early in the week. Worse, you wake up in the middle of the night and peep at your business’ website on your phone to see what your US transactions are doing.

The cause of this current chaos is three catastrophes that have unfolded in the last six months. Governments and central banks around the world overstimulated the global economy in response to the pandemic that caused inflation. Demand was more than supply could handle, resulting in more than “temporary” inflation. So central banks with zero interest rates were miles behind. That was the first leg of a three-game winning streak. The second footprint was the invasion of Ukraine, which sent energy and food prices skyrocketing, further increasing inflationary pressures. And to complete a trifecta, China’s decision to lock down entire cities for months to keep the virus out has exacerbated supply chain problems and further accelerated inflation.

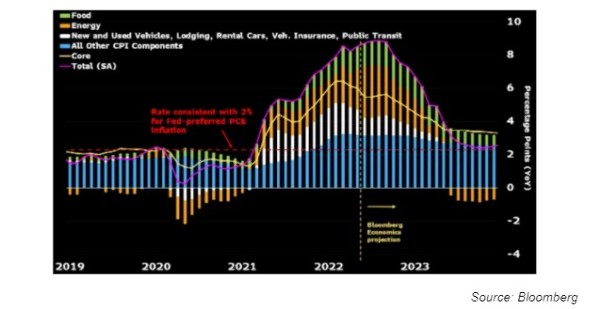

Chart showing rising US CPI

The chart above really visualizes the problems created by the fateful trifecta. This shows the monthly US inflation rate. You can see the deflationary pressures governments and central banks have been dealing with in his 2020. Energy prices have fallen due to lockdowns and travel restrictions. We can then see a steady increase from 2021 to 2022. The latest figures for this month show annual inflation hovering at 8.6% and is projected to reach 9% in the coming months. Then, as we enter 2023, inflation is expected to finally start to slow.

The easing is expected to be very rapid as the sharp rise in the first half of this year will be difficult to replicate in the future. A silver lining to the picture is that inflation has picked up so quickly that it could go back down quickly. Especially if central banks are able to set monetary policy halfway and bring supply and demand closer to some kind of equilibrium. And they’ve been trying to do just that in recent months, with the European Central Bank making a move early next month that will see more than 60 central banks around the world hike interest rates in 2022. The concerted and far-reaching nature of these moves demonstrates a global determination to bring inflation under control. Another aspect of this move is how quickly central banks are raising rates. This month, the US Federal Reserve Board rose 0.75%. It was his first move in 28 years and the funding rate saw him rise to 1.75%. As currently expected, a further 0.75% move at the next meeting would bring the funding rate to 2.5%. The road ahead is starting to look like interest rates will rise to 3-4%, depending on the country, and inflation will fall to 3-4%, depending on the country, in the first quarter of next year. .

If central banks prove to be able to control inflation by early next year, the damage caused by the trifecta of fate should ease. It’s also worth noting that the market tends to look six to nine months ahead. This means that volatility could ease as we move into the second half of 2022, if this appears to be the path forward. The global economy is holding up as demand is expected to cool. But that’s a matter of 2023, and for now, most investors will likely settle for a little more kindness in late 2022.

Disclaimer

The following commentary represents the opinion of the author only. The views expressed are provided for informational purposes only and should not be construed as an offer, endorsement or solicitation to invest. All materials presented are believed to be reliable, but their accuracy cannot be certified. The opinions expressed in these reports are subject to change without notice. Castlepoint may or may not invest in any of the securities mentioned.

About Castle Point Fund Management Limited

Castlepoint is a New Zealand boutique fund manager founded in 2013 by Richard Stubbs, Stephen Benny, Jamie Young and Gordon Sims. Castlepoint’s investment philosophy focuses on long-term opportunities and investor alignment. Castlepoint has been named Morningstar Fund Manager of the Year 2021 – Domestic Equities.

About Stephen Benny

Stephen is the co-founder of Castle Point. He has over 25 years of investment experience in New Zealand and abroad and over 18 years of portfolio management experience. Stephen holds a Bachelor of Arts Honors in Business Studies and Accounting from the University of Edinburgh in 1991 and is a CFA credential holder.

Stock photos can be found here:

For more information, see:

http://www.castlepointfunds.com

Comments from readers

No comments yet

login To add a comment

https://www.goodreturns.co.nz/article/976520863/could-2022-get-better-from-here-it-s-certainly-hard-to-get-worse.html?utm_source=GR&utm_medium=rss&utm_campaign=Could+2022+get+better+from+here%2C+it%E2%80%99s+certainly+hard+to+get+worse 2022 is certainly hard to get better or worse from here